Managing a law firm requires more than legal expertise. It demands strict financial discipline and compliance with rules that most businesses never face.

Unlike general business accounting, legal accounting comes with unique complexities. You’re dealing with trust accounts, IOLTA compliance, client funds, and strict ethical obligations that can result in significant financial penalties if mishandled.

Legal accounting isn't just about tracking profit. It's about maintaining compliance with state bar rules, protecting client funds, and building a foundation for sustainable growth.

This guide walks you through everything you need to know about accounting for law firms. Whether you manage accounting yourself or work with a professional, understanding these basics helps protect your practice and support long-term growth.

Key Takeaways

- Law firm accounting is a specialized financial management process that ensures compliance with bar associations and regulatory authorities.

- Trust accounting is the most critical compliance obligation for law firms, requiring client funds to be kept completely separate from operating funds.

- Legal-specific accounting tools support trust compliance and accurate billing, features that general accounting software lacks.

- A legal accountant understands the unique financial practices of law firms and can provide tax savings, compliance protection, and time savings.

What Is Law Firm Accounting?

Law firm accounting refers to the financial management practices specific to legal practices. It is a specialized system for recording financial transactions, managing trust accounts, preparing financial statements, and ensuring compliance with legal accounting rules established by state bar associations and regulatory authorities.

This system adds additional layers of compliance beyond standard business accounting. It requires strict separation of client funds from operating funds and adherence to professional responsibility rules.

Why It Matters

Accurate financial records help you run a profitable practice and maintain healthy cash flow. They allow you to see which practice areas generate revenue and which ones cost you. This insight supports informed business decisions about where to invest resources and where improvements are needed.

Proper accounting for law firms protects you from serious consequences. Violating legal accounting rules can result in license suspension, malpractice claims, and significant financial penalties.

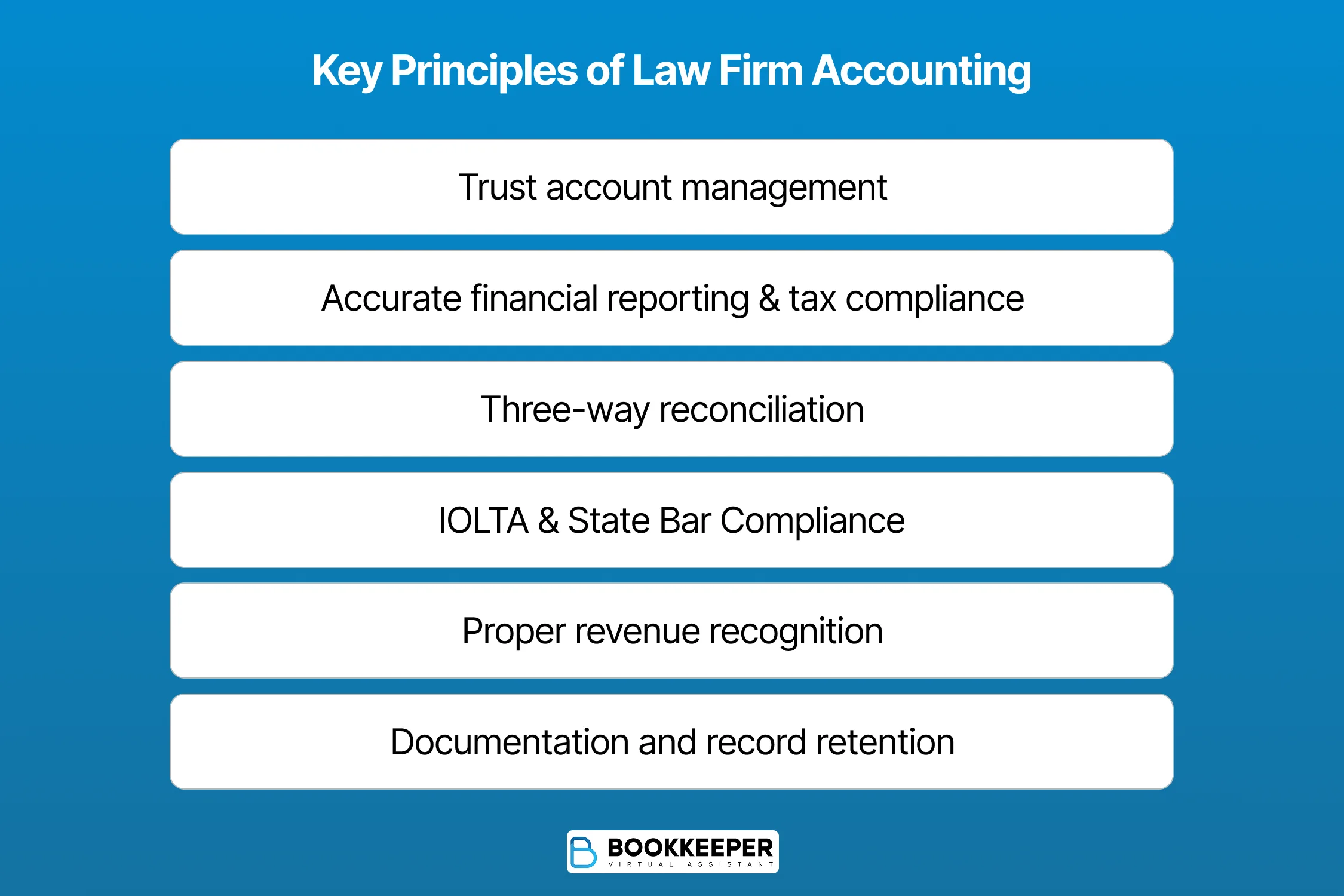

Key Principles of Law Firm Accounting

Law firm accounting operates under specific principles that set it apart from general business accounting.

- Trust account management requires complete separation between client funds and operating funds at all times.

- Accurate financial reporting ensures reliable data for tax obligations, business planning, and regulatory compliance.

- Three-way reconciliation is required for trust accounts. Each month, you must reconcile your bank balance, your trust ledger balance, and the total of all individual client ledger balances.

- IOLTA compliance requires proper handling of client funds held in trust, including depositing eligible funds into approved accounts and maintaining detailed records in accordance with state bar rules.

- Proper revenue recognition requires that unearned retainers remain in trust until earned and be transferred to the operating account only as services are performed.

- Documentation and record retention require law firms to maintain financial and trust records for the period mandated by their jurisdiction, typically five to seven years.

Law Firm Accounting vs. Bookkeeping

Law firm bookkeeping involves the day-to-day recording of financial transactions. This includes data entry for income and expenses, bank reconciliations, categorizing transactions, and maintaining organized financial records.

Law firm accounting takes bookkeeping data and uses it for analysis, compliance, and planning. Accountants prepare financial statements, handle tax obligations, ensure regulatory compliance, and evaluate overall financial performance.

Bookkeeping records financial activity. Accounting interprets that data, ensures compliance, and supports decision-making. Most law firms need both functions working together for effective financial management.

Trust Accounting for Lawyers

Trust accounting represents the most critical—and most regulated—aspect of law firm accounting. When you hold client funds, you accept a fiduciary responsibility that requires thorough record-keeping and strict compliance with state bar rules.

IOLTA Accounts

Interest on Lawyers' Trust Accounts (IOLTA) hold client funds that are nominal in amount or held for short periods. The interest earned goes to fund legal aid programs rather than to the firm or client. IOLTA accounts are mandatory in most jurisdictions for handling client retainers and settlement funds.

Escrow Accounts

Escrow accounts hold larger sums or funds held for extended periods where interest benefits the client. These accounts are typically used in real estate transactions, large settlements, or when a client specifically requests interest-bearing treatment of their funds.

When to Use IOLTA vs. Escrow

Use IOLTA accounts for retainers, advance fee deposits, and funds held briefly during transactions. Use escrow accounts when client funds are substantial enough to generate meaningful interest or when holding periods extend beyond a few months. Your state bar rules will provide specific thresholds.

ABA Rule 1.15: Model Rules of Professional Conduct

ABA Rule 1.15 establishes the foundation for trust account management. It requires attorneys to hold client property separate from their own, maintain complete records of all trust account transactions, and promptly deliver funds when due.

Attorneys should familiarize themselves with both the ABA Model Rules and their state’s specific implementation, as trust accounting requirements vary by jurisdiction.

Key Trust Accounting Rules

- Never borrow from an IOLTA: Using client funds for firm expenses—even temporarily—constitutes misappropriation and grounds for disbarment.

- Keep trust and business accounts separate: Maintain distinct business bank accounts and trust accounts. Never commingle client funds with your operating account.

- Never record trust deposits as income: Client funds in trust are not revenue until earned. Recording a trust deposit as income creates both accounting errors and compliance violations.

Three-Way Trust Reconciliation

Three-way reconciliation compares three balances: your bank statement balance, your trust account ledger balance, and the total of all individual client ledger balances. All three amounts must match exactly.

This reconciliation should be performed at least monthly, although many firms complete it weekly to reduce risk.

Any discrepancy signals an error that must be investigated and corrected immediately. Common causes of trust reconciliation mistakes include data entry errors, timing differences between deposits and withdrawals, unrecorded bank fees, and incorrect client ledger postings.

Accounting Methods for Law Firms

Choosing the right accounting method affects how you recognize accounts receivable, when you pay taxes, and how accurately your financial statements reflect your firm's performance.

Cash Basis Accounting

Cash basis accounting records income when you receive payment and expenses when you pay them. This method offers simplicity and provides a clear picture of actual cash flow. It works well for solo practitioners and small law firms with straightforward billing structures.

Consideration: Cash accounting doesn't show work performed but not yet billed, or invoices sent but not yet paid. You may have a healthy bank balance while sitting on unbilled or uncollected work.

Accrual Basis Accounting

Accrual accounting records income when it is earned (work completed) and expenses when they are incurred (services received), regardless of when cash changes hands.

This method provides a more accurate picture of your firm’s overall financial health and is required for firms exceeding certain IRS revenue thresholds.

Consideration: You may owe taxes on income you have not yet collected. Accrual accounting also requires more sophisticated tracking and reporting systems.

Which Method Fits Your Firm

Solo practitioners and small law firms often start with cash basis accounting for its simplicity. As firms grow, accrual accounting provides better insight into true profitability. Larger firms typically use accrual accounting for more accurate financial reporting.

Some firms consider using a modified cash approach, which applies cash basis accounting for most transactions but incorporates limited accrual tracking for specific items such as accounts receivable.

This approach lets you track outstanding client balances without paying taxes on money you haven't received yet.

Common Legal Accounting Mistakes To Avoid

Even experienced attorneys make accounting errors that create compliance issues and financial problems. Understanding common legal accounting mistakes allows you to implement safeguards before small issues turn into serious violations.

- Commingling funds: Mixing client funds with operating funds is the fastest path to disciplinary action. Maintain strict separation between trust accounts and your business operating account at all times.

- Neglecting reconciliations: Skipping monthly trust reconciliations allows errors to compound. Small discrepancies can quickly become major compliance problems.

- Mixing personal and business expenses: Using a business credit card for personal purchases (or vice versa) creates tax complications and increases audit risk. Keep personal and business finances completely separate.

- Poor accounts receivable management: Failing to track and follow up on outstanding invoices weakens cash flow and reduces profitability. Implement systematic billing and collection procedures.

- Inadequate record retention: Most jurisdictions require financial records to be maintained for five to seven years. Establish clear retention policies and secure backup systems.

- Recording retainers as income: Unearned retainers must remain in trust, not on your income statement. Funds should only be transferred to your operating account as they are earned.

- Ignoring state-specific requirements: Trust accounting rules vary by state. Ensure your accounting practices align with your jurisdiction’s specific bar regulations.

Accounting mistakes are rarely intentional, but they can carry serious consequences. Establishing strong internal controls and working with a legal accounting professional can significantly reduce these risks.

Legal Accounting Software & Technology

The right legal accounting software simplifies compliance and reduces errors. However, not all accounting platforms meet the unique requirements of law firms. Any solution you choose must properly support trust accounting, client billing, and bar compliance—areas general accounting software often fails to address.

Legal accounting solutions range from standalone platforms built for attorneys to legal-specific add-ons for popular accounting programs. Here are several options to consider:

- Clio: A comprehensive practice management platform with integrated legal accounting features. Clio offers trust accounting, billing, and financial reporting designed specifically for law firms. It also provides strong integration capabilities with third-party tools.

- CosmoLex: An all-in-one legal accounting platform with built-in trust accounting compliance. CosmoLex eliminates the need for QuickBooks by combining legal-specific accounting with practice management features.

- MyCase: Practice management software with integrated accounting features including trust accounting, online payments, and financial reporting. It is known for its user-friendly interface and strong client communication tools.

- LeanLaw: Legal accounting software designed to work with QuickBooks Online while adding necessary law firm features. LeanLaw provides the trust accounting and compliance layer that QuickBooks lacks.

Pro tip: Take advantage of vendor demos and free trials before committing. Test how each platform handles your specific workflow, especially trust accounting and billing processes.

Payments, Billing & Payroll For Law Firms

How your law firm accepts payments directly affects cash flow, client satisfaction, and accounting complexity. Establish clear payment policies and infrastructure from the start.

Offering multiple ways to pay reduces friction and speeds up your collection cycle:

- Credit & Debit Cards: Most clients expect this option, allowing for immediate payment upon receipt of an invoice.

- ACH Transfers: A cost-effective alternative to checks for larger payments, with lower transaction fees. Transfers typically process within 1–3 business days.

- Online Payment Portals: Secure web or mobile platforms that allow clients to view balances and pay 24/7 at their convenience.

- Traditional Methods: Many firms still offer checks and wire transfers for clients who prefer them.

The right payment and billing provider can automate invoicing, reduce errors, and improve cash flow for your practice.

Tax & Compliance Obligations

Law firms face the same tax obligations as other businesses, plus industry-specific compliance requirements. Staying current requires systematic attention throughout the year.

Here are the taxes legal practices commonly need to pay:

- Federal income tax: Based on your firm's structure—sole proprietors report on Schedule C, partnerships file Form 1065, and corporations file Form 1120 or 1120-S.

- State income tax: Most states require income tax filings, with rates and rules varying by jurisdiction.

- Self-employment tax: Solo practitioners and partners pay Social Security and Medicare taxes on net self-employment income, currently 15.3% according to the IRS. This does not apply to C corporation owners and applies differently to S corporation owners.

- Quarterly estimated taxes: Required at the federal level if you expect to owe $1,000 or more; state requirements vary.

- Payroll taxes: Firms with employees must withhold and remit federal income tax, Social Security, Medicare, and state income taxes, plus pay employer portions of FICA and unemployment taxes.

- State unemployment tax (SUTA): Required for firms with employees, with rates varying by state and your firm's claims history.

- Sales tax: Some states require sales tax on certain legal services—check your state's specific requirements.

- Franchise or business privilege tax: Several states impose annual taxes simply for the privilege of doing business, regardless of profitability.

Beyond taxes, law firms must also comply with state bar trust account rules, IOLTA program requirements, and record retention policies. Proper documentation of the business purpose for each expense is important to support both tax filings and potential bar audits.

When to Hire a Legal Accountant

While you can handle basic bookkeeping in-house, professional accounting support provides significant advantages. A legal accountant brings specialized expertise in trust account compliance, tax strategy, and financial planning—areas most attorneys don’t have the time to manage deeply.

They understand the nuances of IOLTA requirements, proper revenue recognition for retainers, and the unique cash flow challenges law firms face.

Consider hiring a legal accountant when your firm reaches the point where:

- Tax complexity exceeds your comfort level

- Trust account reconciliations consume too much of your time

- You’re considering changes to your firm structure

- You need more time to focus on practicing law

The cost of professional accounting services often pays for itself through tax savings, avoided compliance issues, and the peace of mind that comes from knowing your books are audit-ready.

Choosing Law Firm Accounting Services

Look for accounting services that specialize in working with law firms. They should understand attorney trust account rules, legal ethics requirements in your state, and proper trust reconciliation procedures.

Bookkeeper.law specializes in connecting law firms with legal bookkeepers who become a direct part of their team to handle accounting and bookkeeping. Our professionals are vetted for legal accounting experience and understand the unique financial and compliance demands attorneys face.

Best Practices for Law Firm Accounting

Implementing consistent accounting practices protects your firm and sets a foundation for growth. These best practices apply whether you're a solo practitioner or managing a larger firm.

- Reconcile trust accounts monthly: Complete three-way reconciliation of all trust accounts every month without exception. Investigate and resolve discrepancies immediately.

- Separate all firm bank accounts: Maintain distinct accounts for operations, trust, and taxes. Never use personal accounts for business transactions.

- Use legal-specific accounting software: Invest in software designed for law firms rather than adapting general accounting tools. The compliance features justify the cost.

- Document everything: Maintain records of all financial transactions with supporting documentation. Good records simplify tax filing and protect you during audits.

- Review financial statements regularly: Examine your balance sheet, income statement, and cash flow reports monthly. Understanding your firm's financial health enables better decisions.

- Set aside money for taxes: Transfer a percentage of every payment received to a dedicated tax account. This prevents scrambling when quarterly payments come due.

- Stay current on compliance requirements: Trust accounting rules and tax laws change. Subscribe to bar association updates and work with professionals who stay current.

Build relationships with accounting professionals: Don't wait for a crisis to find a bookkeeper or CPA. Establish these relationships proactively so help is available when needed.

Conclusion

Effective law firm accounting comes down to compliance, accuracy, the right tools, and professional support when needed. Master your trust accounting obligations, invest in legal-specific software, and consider bringing in a legal accountant as your practice grows.

Your legal practice deserves accounting practices as rigorous as the work you do for clients. The time and resources you invest in building systems that follow best accounting practices protect your license and position your firm for long-term success.

Frequently Asked Questions

Does a law firm need an accountant?

While not legally required, most law firms benefit from professional accounting support. An accountant helps ensure trust account compliance, optimize tax strategy, and free you to focus on practicing law.

What are law firm accounting services?

Law firm accounting services include bookkeeping, trust (IOLTA) accounting, billing and invoicing, payroll, tax preparation, financial statement preparation, accounts receivable and payable management, and compliance support. These services may be provided by in-house staff, outsourced bookkeepers, or CPAs.

What accounting method do most law firms use?

Most small to mid-sized law firms use the cash basis method, where income is recorded when received and expenses when paid. Firms with average annual gross receipts over $25 million are generally required by the IRS to use the accrual method. Some firms adopt accrual earlier for more accurate financial reporting.

Can law firms use QuickBooks for accounting?

Yes, law firms can use QuickBooks for bookkeeping and financial reporting. However, it lacks legal-specific features for trust accounting and does not natively support three-way reconciliation. If you choose QuickBooks, consider pairing it with legal-specific software that provides proper trust account support.