As a legal professional, managing client funds is a complex process that requires the right expertise and strict compliance. Even a very small error—one you might think doesn’t matter—still does. It needs to be perfect and accurate.

Mixing your client’s money with your personal finances is not only a bad practice, but it also often involves serious legal and ethical consequences. A trust account plays an essential role in helping law firms manage these situations properly.

Whether you're just starting your practice or looking to refresh your knowledge, this guide will walk you through everything you need to know about trust accounts, from basic definitions to practical considerations.

Defining Trust Account

A trust account is a special type of bank account used by a trustee to hold funds or assets for the benefit of the beneficiary. In the legal context, it's where you keep client funds that you haven't yet earned or that you're holding for a specific purpose related to legal representation.

Think of a trust account as a financial safekeeping box. The money in this account legally belongs to your clients or third parties—not to you or your firm—until you've earned it or until it needs to be disbursed according to client instructions.

Important Trust-Related Terms You Should Know

When dealing with trust accounts, you'll encounter several important terms that are essential to understand:

Trustee: A trustee is the person responsible for managing the trust account and its assets. As a legal professional, you act as a fiduciary with a legal obligation to manage funds in the best interest of the client, following specific rules about usage and disbursement.

Grantor: The grantor is the person who creates the trust and provides the funds or assets to be held. They are primarily responsible for setting the terms of the trust, deciding who the beneficiaries are, and defining how the funds should be managed and distributed.

Beneficiary: The beneficiary is the person who benefits from the money in the trust. This is usually your client, but sometimes it includes third parties. Multiple beneficiaries might have interests in different portions of the same trust account, and all beneficiaries have the right to accountings and information about their funds.

Reconciliation: It is the process of ensuring that three sets of records match: your internal client ledger, your trust account journal, and your bank statement. It is typically performed monthly and is required by most bar associations to identify and resolve any errors or discrepancies early.

Fiduciary Duty: This means you must always act in the best interest of your client. You must avoid conflicts of interest, never use trust funds for personal benefit, and exercise reasonable care in protecting and managing the funds.

Escrow: Escrow refers to funds held for a specific transaction that are released only when predetermined conditions are met. In real estate law, escrow accounts are commonly used to hold earnest money deposits, and escrow agents have defined responsibilities regarding the funds they manage.

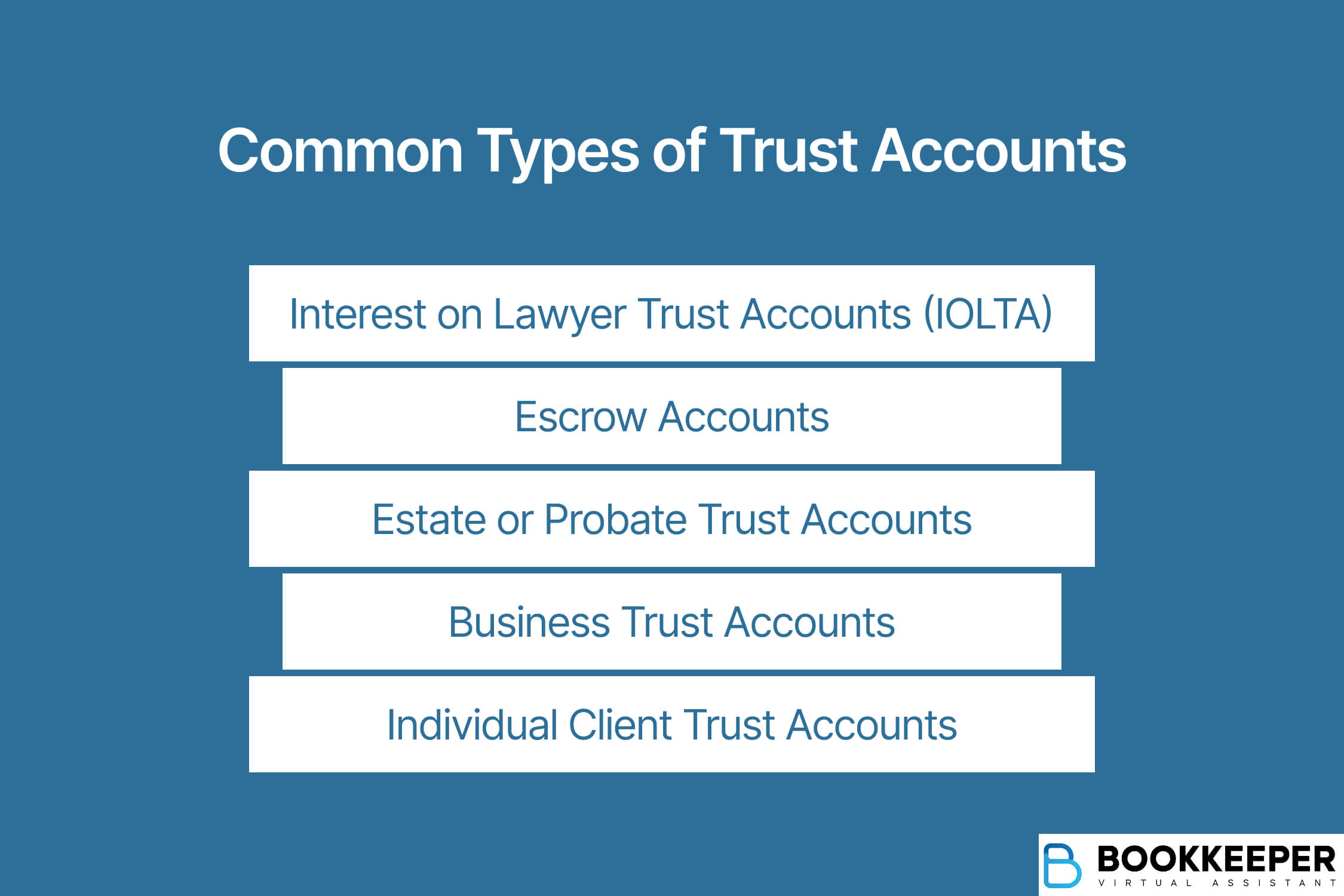

Types of Trust Accounts

Not all trust accounts are created equal. Depending on your practice area and jurisdiction, you might need to set up different types:

Interest on Lawyer Trust Accounts (IOLTA)

An account used by attorneys to hold client funds separately from their own. IOLTA accounts pool small or short-term client funds to earn interest, which supports legal aid and public service programs through state bar foundations.

Escrow Accounts

Used mainly in real estate, escrow accounts temporarily hold funds until certain agreed-upon conditions are met.

Estate or Probate Trust Accounts

These accounts are used to manage and protect a deceased person’s assets during the probate process. They ensure debts are paid and distributions to beneficiaries follow the terms of the will or applicable state law.

Business Trust Accounts

Businesses hold client or vendor funds in trust accounts until certain conditions are met, such as customer payments or deposit.

Individual Client Trust Accounts

Used when client funds are substantial or held long-term, these accounts are interest-bearing and set up under the client’s name or tax ID.

What is the purpose of a trust account?

The main purpose of a trust account is to keep other people’s money separate from your personal and business funds. This separation prevents client money from being used for firm expenses, protects it from your firm’s creditors, and avoids the prohibited commingling of funds.

It also builds trust with clients, courts, and regulatory agencies. By maintaining detailed records and handling client funds properly, you show a commitment to ethical practice and avoid the serious consequences of mishandling client money.

Benefits and Risks of Having Trust Accounts

Benefits

- Clear Financial Boundaries: Trust accounts create a clear separation between your money and client funds, reducing confusion and potential conflicts.

- Client Confidence: Clients feel more secure when they know their funds are held separately and securely.

- Regulatory Compliance: Well-maintained trust accounts keep you in good standing with your state bar and regulatory authorities.

- Professional Risk Management: Proper trust accounting protects you from accusations of financial impropriety.

- Transparency: Clear record-keeping makes it easier to show where the money came from and how it was used.

Risks

- Accounting Mistakes: Even minor errors can have serious consequences, including bar complaints and disciplinary actions.

- Administrative Burden: It requires meticulous record-keeping and regular reconciliation. It can take up a lot of your time, especially if you're focused on client work. This is where a specialized legal bookkeeper, like the team at Bookkeeper.law, can make a big difference.

- Potential Penalties: Mismanagement of trust accounts, even if unintentional, can result in sanctions, fines, or even license suspension.

- Technical Complexity: It has rules that can be complex and vary by jurisdiction, requiring careful attention to detail.

How Much Money Do You Need to Open a Trust Account?

You can establish a trust with any amount of funds and assets, as long as they hold value and can be legally transferred into the trust. There is no minimum required amount to establish a trust account.

However, it's important to consider whether setting one up makes sense, especially if the cost or complexity of transferring the assets outweighs the benefits. According to data from the Federal Reserve, the median size of a trust fund is around $285,000.

For lawyers, the minimum amount to open a trust account (such as an IOLTA) depends on the bank. Most banks allow you to open one with an initial deposit as low as $100.

However, there may be additional costs beyond the initial deposit, such as monthly maintenance fees or a minimum balance requirements.

If you're setting up a legal trust account, it's recommended to check with your state bar or local regulations, as they often provide specific setup guidelines and lists of approved banking partners.

Is it worth it to have a trust account?

Yes. For legal professionals, trust accounts aren’t optional—they’re a required part of ethical and compliant practice management. Beyond regulatory compliance, trust accounts provide clear financial separation between your funds and your clients’, reducing the risk of ethics violations or malpractice claims.

Trust accounting keeps you compliant with bar regulations and significantly reduces the risk of ethics complaints or malpractice claims.

However, managing trust accounting on your own can be overwhelming. Instead of focusing on billable work, you may find yourself bogged down by administrative tasks. At Bookkeeper.law, our legal bookkeepers have helped thousands of law firms nationwide establish and maintain compliant trust accounting systems. We understand the challenges that come with managing client funds and handle the technical details so you can focus on practicing law.

Ready to simplify your trust accounting? Sign up today to get started.