Running a successful law firm involves more than strong case strategy and excellent client service. To remain profitable and sustainable, firms must also stay on top of their financial management. While taxes can feel like an unavoidable headache for busy law firm owners, smart planning can turn them into a manageable and strategic part of your business.

A well-structured tax strategy can help reduce taxable income, lower overall tax liability, and improve financial efficiency. In this guide, we’ll break down 13 practical tax planning strategies that law firms of all sizes can use to keep more of what they earn—without getting lost in complex financials.

What Is Tax Planning for Law Firms?

Tax planning is the process of analyzing a law firm’s financial situation to comply with tax laws while minimizing tax obligations. It involves making strategic decisions about income timing, expense deductions, business structure, and other financial factors to reduce taxes owed.

Unlike tax preparation, which focuses on filing tax returns after the year ends, tax planning happens throughout the year. Many law firms work with accountants or tax professionals who specialize in legal industry finances to identify deductions and credits specific to their practice areas and operations.

Understanding Tax Liabilities

Tax liabilities are the legal obligations of an individual or business to pay taxes to government authorities based on taxable income, transactions, or other taxable events.

A tax liability is not simply a percentage of revenue. It is calculated after applying deductions and credits to gross income. Tax liabilities differ from taxes already withheld or estimated payments made during the year.

If total liability exceeds payments, the firm must pay the difference; if payments exceed liability, the firm may receive a refund. Unpaid tax liabilities can result in penalties, interest, or collection actions by tax authorities.

What Creates Tax Liabilities for Law Firms

Several factors contribute to your firm's tax obligations:

- Fee income and billable revenue – Most taxable income comes from client fees, whether charged hourly, as a flat rate, or on a contingency basis.

- Partnership distributions and owner compensation – The way partners and owners are paid affects both the firm’s and individuals’ tax situations.

- Investment and interest income – Interest earned on IOLTA accounts, client settlements held in trust, or firm investments can generate taxable income.

- Capital gains – Selling firm assets, equipment, or property may trigger capital gains taxes.

- Payroll obligations – Employee wages create payroll tax responsibilities, including Social Security, Medicare, and unemployment taxes.

- State and local taxes – Depending on the firm’s location, additional state income taxes, franchise taxes, or local business taxes may apply.

12 Smart Tax Planning Strategies to Reduce Tax Liability

1. Choose the Right Business Structure

Your firm's legal structure directly impacts how much you pay in taxes. Each structure comes with different tax implications, liability protections, and administrative requirements.

Many law firms find that S corporation election offers valuable tax advantages by allowing them to save on self-employment taxes by splitting income between a reasonable salary and shareholder distributions. However, the right choice depends on your specific situation, so it’s important to evaluate your options carefully.

2. Maximize Retirement Account Contributions

Retirement contributions offer one of the most straightforward ways to reduce taxable income. Money contributed to qualified retirement plans is typically deducted from your taxable income, lowering your current-year tax bill while helping you build long-term wealth.

Contributing to a 401(k), SEP IRA, or Defined Benefit Plan reduces your taxable income dollar-for-dollar. In 2026, the Internal Revenue Service (IRS) increased the 401(k) employee contribution limit to $24,500, with a catch-up contribution limit of $8,000 for participants age 50 and older.

The key is consistency. Making regular contributions throughout the year maximizes tax benefits and helps avoid last-minute scrambles.

3. Optimize Timing of Income and Expenses

Strategically timing income and expenses can help shift taxable income between years and reduce overall tax liability. For many law firms that operate on a cash-basis accounting method, deferring year-end client billings until January may lower current-year taxable income if the firm expects to be in a lower tax bracket the following year.

Income timing strategies may include:

- Delaying billing for work completed late in the year until January

- Holding off on depositing client payments received at year-end until the new year, when permissible

- Structuring contingency-fee matters to conclude during tax-advantageous periods

Expense timing strategies may include:

- Prepaying January rent, insurance premiums, or business subscriptions in December

- Accelerating equipment purchases or necessary repairs into the current year

- Paying annual bar dues, licensing fees, and professional memberships before year-end

This strategy is most effective when there are expected changes in income levels or tax rates between years. For example, if higher earnings are anticipated next year, accelerating income into the current year may be beneficial. Conversely, during a high-income year, deferring income and accelerating deductions can help reduce tax exposure.

4. Use the Qualified Business Income (QBI) Deduction

Under the Tax Cuts and Jobs Act (TCJA), eligible self-employed individuals and small business owners may claim a deduction of up to 20% of qualified business income (QBI) from pass-through entities such as partnerships, S corporations, and sole proprietorships.

Although law firms are classified as Specified Service Trades or Businesses (SSTBs), firm owners may still qualify for the QBI deduction if their total taxable income falls below IRS-established thresholds. Once income exceeds those limits, the deduction is reduced or eliminated.

5. Take Advantage of Technology and Equipment Deductions

The tax code offers incentives that allow law firms to recover the cost of business equipment and technology more quickly than through traditional depreciation. One commonly used option is Section 179, which permits businesses to deduct the cost of qualifying assets in the year they are placed into service, subject to annual IRS limits.

Qualifying purchases often include:

- Computers and laptops

- Software

- Office furniture and fixtures

- Printers, scanners, and related equipment

- Machinery and other qualifying business assets

These deductions can significantly reduce taxable income in the year of purchase, making them especially valuable for firms investing in operational efficiency or technology upgrades.

6. Implement PTE Tax Elections (SALT Cap Workaround)

Many states now allow a Pass-Through Entity (PTE) tax election, which enables law firms to pay state income taxes at the entity level rather than at the individual partner level.

Because these entity-level taxes are generally treated as deductible business expenses for federal tax purposes, this approach can bypass the $10,000 federal cap on State and Local Tax (SALT) deductions.

Partners typically receive a corresponding credit or adjustment on their state returns for taxes paid by the firm.

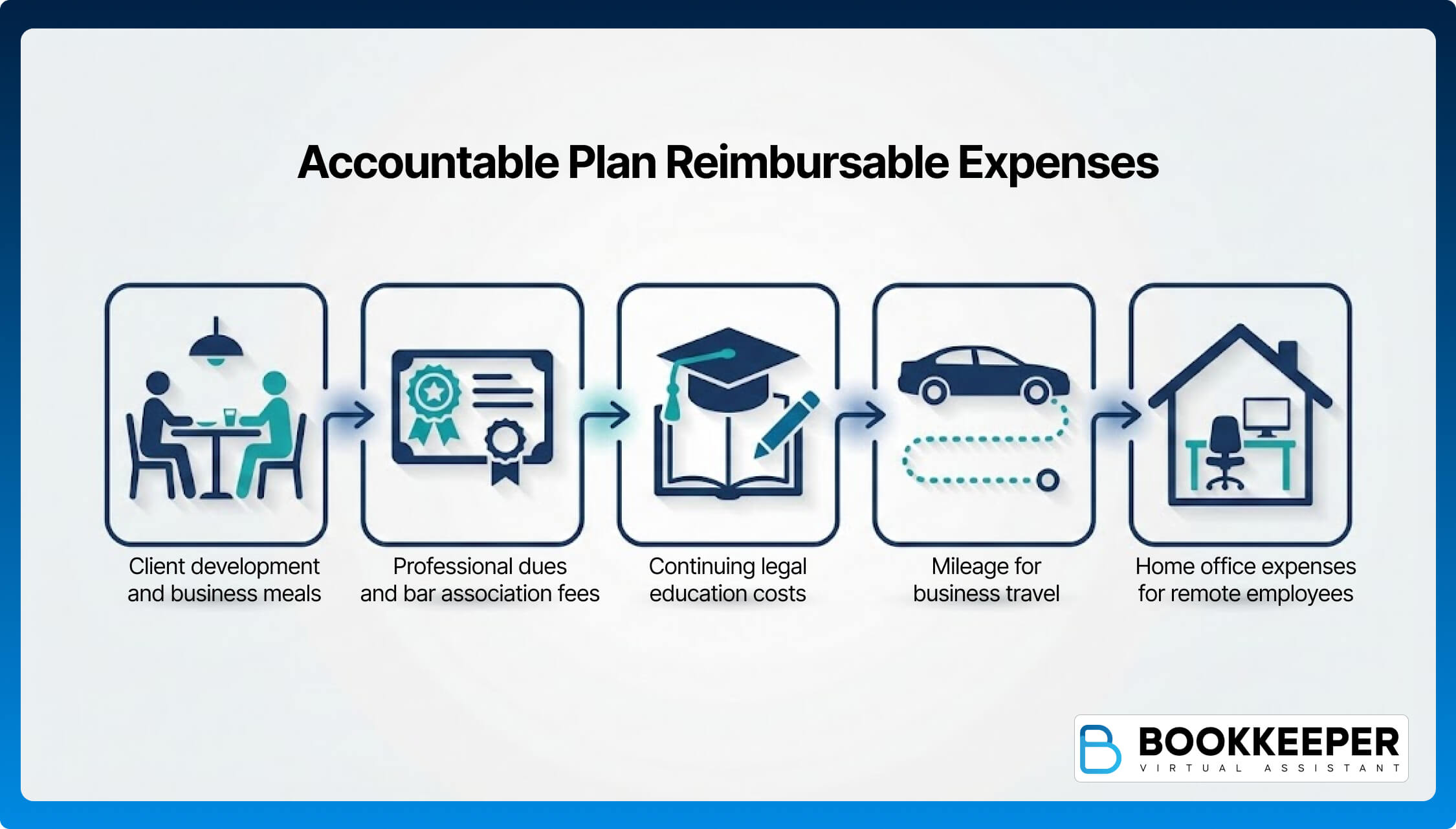

7. Establish Accountable Expense Reimbursement Plans

An accountable plan allows your firm to reimburse employees and partners for business expenses without those reimbursements counting as taxable income. This creates tax savings for both the firm and individuals.

To qualify as an accountable plan, the arrangement must meet key requirements:

- Expenses must have a business connection

- Expense must be substantiated with receipts or records

- Any excess reimbursements must be returned to the firm

Common reimbursable expenses under an accountable plan include:

- Client development and business meals

- Professional dues and bar association fees

- Continuing legal education costs

- Mileage for business travel

- Home office expenses for remote employees

Without an accountable plan, reimbursements are treated as taxable compensation, increasing payroll taxes and individual income taxes unnecessarily.

8. Leverage Health Insurance and Fringe Benefits

Premiums for health, dental, and long-term care insurance for partners and employees are generally deductible business expenses. Self-employed attorneys can typically deduct 100% of health insurance premiums for themselves and their families, reducing taxable income.

Law firms can also offer Health Savings Accounts (HSAs) in combination with high-deductible health plans, which provide triple tax benefits:

- Contributions are deductible from taxable income.

- Investment growth is tax-free while funds remain in the account.

- Qualified withdrawals are tax-free when used for eligible medical expenses.

Offering these benefits not only generates tax savings but also helps attract and retain top legal talent, making them a valuable component of a law firm’s compensation and benefits strategy.

9. Deduct Professional Development and Education

The costs of Continuing Legal Education (CLE), bar dues, and legal seminars are generally fully deductible as business expenses. Staying current in your field and maintaining technical skills is considered a business necessity, so it’s important to track these expenses.

Deductible professional development expenses include:

- CLE course fees and materials

- Bar association seminars and conferences

- Legal publications and subscriptions

- Webinars and online training programs

- Travel expenses related to educational events

To qualify, the education must relate to your current practice area or help you maintain your professional license. Expenses for entering a new profession or fulfilling minimum requirements for your current position do not qualify.

Don’t overlook informal education either. Books, podcasts, and online resources that support law practice management, client development, or legal technology can also qualify as deductible business expenses.

10. Consider Charitable Giving

Law firms can reduce their taxable income through charitable contributions, which can take several forms:

- Cash contributions to qualified 501(c)(3) charities

- Donating appreciated securities or property instead of cash, which can provide additional tax advantages by avoiding capital gains taxes

- Deducting out-of-pocket expenses incurred while providing pro bono legal services, such as filing fees or materials

To qualify, contributions must go to eligible organizations and be properly documented. Consistent charitable giving can provide both tax benefits and strengthen a firm’s reputation in the community.

11. Claim Bad Debt Write-Offs

Uncollectible client accounts can provide tax benefits, preventing “phantom income” from increasing your taxable earnings on money you never actually received. How you handle bad debts depends on your firm’s accounting method:

- Cash-Basis Firms: Most law firms use cash-basis accounting, under which unpaid invoices are generally not deductible because income is only recognized when received. However, you can deduct actual out-of-pocket costs advanced on behalf of clients that become uncollectible.

- Accrual-Basis Firms: Firms using accrual accounting recognize income when billed, so bad debts can be deductible if the amount is truly uncollectible. To claim the deduction, you must demonstrate genuine collection efforts and show that the debt is worthless.

For all firms, keep thorough records of your attempts to collect outstanding debts. This may include sending reminder letters, making phone calls, and retaining all correspondence. Proper documentation supports your deduction if it is ever questioned by the IRS.

12. Work with a Tax Specialist

One of the most valuable tax planning strategies may be the simplest: partnering with a qualified tax professional. Tax law is complex, and the rules affecting law firms require specialized expertise to minimize risk and maximize savings.

Look for a tax specialist with experience serving law firms, as their knowledge of the unique nuances of legal accounting can uncover deductions and strategies that a generalist might miss. In many cases, the savings achieved through specialized guidance exceed the cost of their services, making this a smart investment.

Simplify Law Firm Tax Planning with Bookkeeper.law

Managing your firm’s finances shouldn’t take time away from practicing law. That’s where specialized support makes a difference.

Bookkeeper.law provides virtual legal bookkeepers who become a dedicated extension of your law firm. From trust accounting to tax preparation that supports smarter planning, they understand the unique needs of legal practices.

By integrating your financial records with expert oversight, tax planning becomes proactive rather than reactive. You’ll have the data you need to make informed decisions about timing, deductions, and strategic investments.

Final Note

Tax planning isn’t about finding loopholes—it’s about understanding the rules and using them strategically to your advantage. By planning and taking action throughout the year, your firm can remain both competitive and profitable.

Investing time in proactive tax planning can compound the benefits over time, positioning your law firm to minimize taxes and make smarter financial decisions.