Key Takeaways

- The accounting cycle is a repeatable six-step process that keeps every financial transaction accurately recorded and reported within a set period.

- Missing even one step, especially adjusting entries, is among the top causes of financial restatements and compliance failures in small businesses.

- Law firms carry unique accounting obligations like trust accounting and IOLTA compliance, making a disciplined accounting cycle non-negotiable.

- Outsourcing the cycle to a virtual bookkeeper trained in legal accounting can reduce overhead by up to 40% while keeping your firm fully compliant.

So, What Exactly Is the Accounting Cycle?

If you have ever wondered where your firm's financial numbers actually come from, this is the answer: the accounting cycle.

The accounting cycle is a structured, repeatable process businesses use to record, classify, summarize, and report every financial transaction over a set accounting period. That period could be monthly, quarterly, or annual depending on your firm's setup.

Think of it as the foundation your firm's financial health is built on. Without it, there is no reliable way to know whether you are profitable, compliant with bar association rules, or ready for tax season.

According to the AICPA, nearly 60% of small business financial errors trace back to improper bookkeeping practices. Most of those errors? They come from a broken or ignored accounting cycle.

Why Law Firms Cannot Afford to Cut Corners Here

Here is the thing: the accounting cycle is not just good practice for law firms. It is a compliance requirement.

Law firms manage client trust accounts (IOLTA), retainer funds, and case-related expenses that must stay completely separate from operating funds. The American Bar Association's Model Rules of Professional Conduct, Rule 1.15, requires attorneys to maintain meticulous financial records of all client funds.

A properly executed accounting cycle helps your firm:

- Stay compliant with state bar trust accounting rules

- Produce accurate profit and loss statements for partner distributions

- Prepare clean books for tax filings and audits

- Catch billing discrepancies before they snowball into bigger problems

Now let's walk through the six steps, one by one.

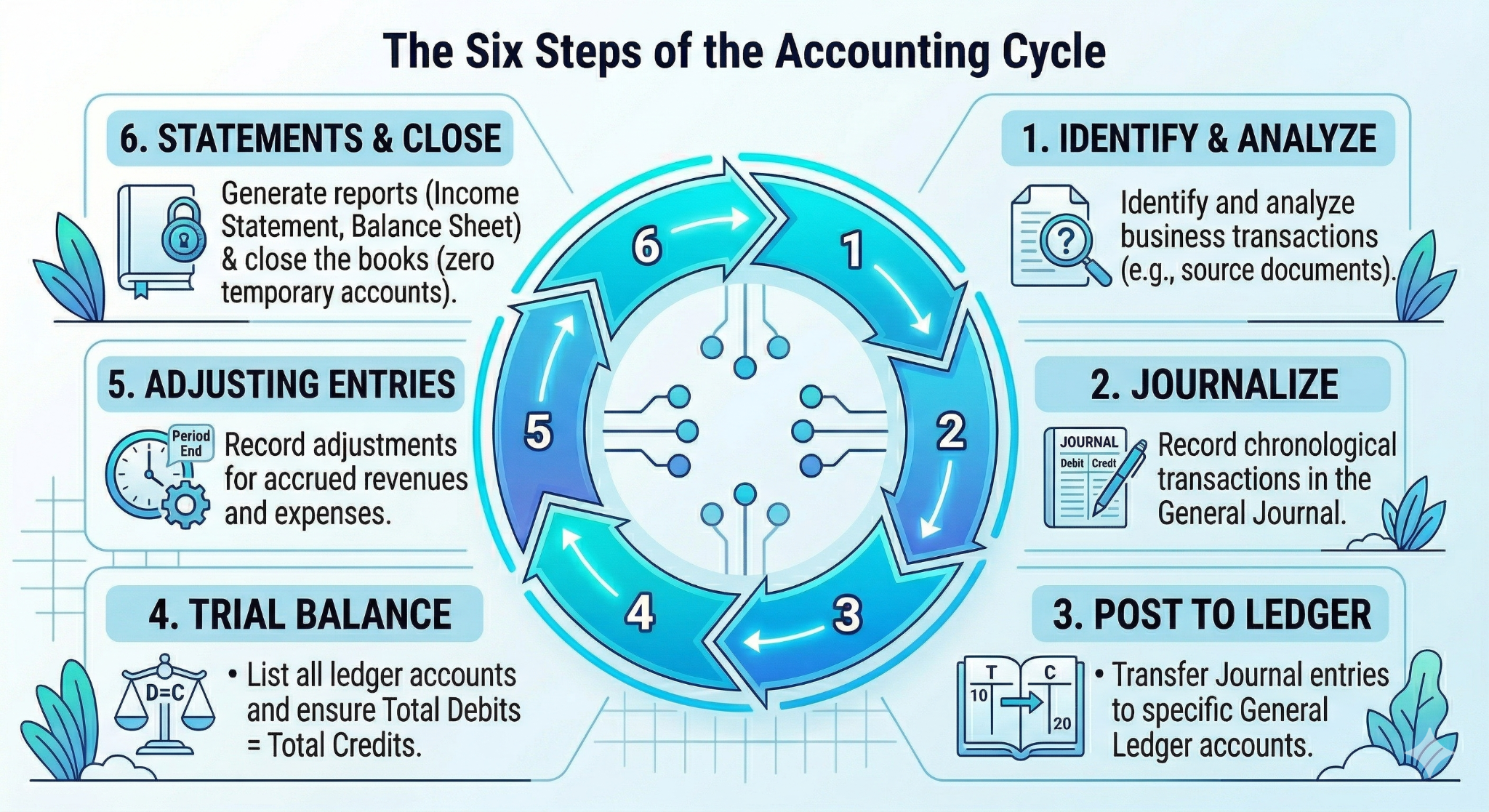

The Six Steps of the Accounting Cycle

Step 1: Identify and Analyze Transactions

Everything starts here. Before anything gets recorded, you need to identify a financial event and understand what it means.

That might be a client retainer received, a court filing fee paid, payroll processed, or an office lease renewed. Each transaction needs to be analyzed to determine:

- Which accounts are affected (cash, accounts receivable, client trust, etc.)

- Whether it is a debit or a credit

- The exact dollar amount and the date it occurred

For law firms, this step also means separating operating funds from client trust funds the moment a transaction is identified. This is where many firms stumble before the cycle even gets going.

Step 2: Record Transactions in a Journal

Once you have identified and analyzed a transaction, it gets recorded chronologically in a general journal as a journal entry. Every entry follows the double-entry bookkeeping rule: every debit must have a matching credit of equal value.

It sounds straightforward, but errors here compound fast. A 2023 report by QuickBooks/Intuit found that 82% of business failures are linked to poor cash flow management, most of which starts with inaccurate journal entries.

Step 3: Post to the General Ledger

After transactions are journalized, they get transferred, or "posted," to the general ledger. This is the master record of every account your firm uses: assets, liabilities, equity, revenue, and expenses.

Each account in the ledger accumulates a running balance as entries are posted. For law firms using software like Clio, QuickBooks, or PCLaw, this step is often automated. But automation does not eliminate the need for a trained eye reviewing the output for accuracy.

Step 4: Prepare a Trial Balance

At the end of the period, all ledger balances are pulled together into a trial balance, a two-column report that confirms total debits equal total credits.

This is your first real checkpoint. If the numbers do not balance, there is an error somewhere in Steps 1 through 3 that needs to be found and fixed before you go any further.

The IRS reports that 21% of small business tax returns contain errors that trace back to unbalanced or poorly maintained ledgers. A clean trial balance at this stage saves enormous headaches later.

Step 5: Record Adjusting Entries

This is the step most firms either rush or skip entirely, and it is one of the most important.

Adjusting entries account for revenues and expenses that occurred during the period but were not captured in the original journal entries. These include:

- Accrued revenue: Legal work that was completed but not yet billed to the client

- Prepaid expenses: Office lease or malpractice insurance paid ahead of time

- Depreciation: The gradual cost allocation of office equipment, computers, or furniture

- Unearned retainer fees: Client funds received for services not yet rendered

Adjusting entries ensure your financial statements reflect the true economic activity of the period under the accrual accounting method, which is required by GAAP for firms above a certain revenue threshold.

Skipping this step does not just produce inaccurate reports. For law firms, it can misrepresent trust account balances and create serious bar compliance exposure.

Step 6: Generate Financial Statements and Close the Books

The final step actually covers two closely related actions: producing your financial statements and then closing out the period.

First, the financial statements. With adjusted balances in place, your firm can now generate its three core reports:

These reports are not just internal documents. They support partner compensation decisions, loan applications, tax preparation, and state bar trust account audits.

Then, close the books. Closing entries reset temporary accounts like revenues and expenses to zero so the next period starts clean. Permanent accounts such as assets, liabilities, and equity carry their balances forward into the new period.

After closing, a post-closing trial balance confirms all temporary accounts are zeroed out and the ledger is ready to go again.

How Long Should the Accounting Cycle Take?

That depends on how well the firm is maintaining records throughout the period. Here is a general benchmark:

A well-run small law firm should be able to close a monthly accounting cycle within 3 to 5 business days after month-end, provided records were kept current throughout the month.

Accounting Cycle vs. Budget Cycle: What Is the Difference?

These two get mixed up often. Here is a quick comparison:

Common Mistakes That Break the Cycle

Even experienced professionals get these wrong. Here are the mistakes that show up most often in law firm books:

- Commingling client funds with operating accounts (a direct bar association violation)

- Missing or skipping adjusting entries, which leads to overstated or understated income

- Not reconciling trust accounts at every period close

- Using cash-basis accounting when accrual-basis is required by GAAP or lender covenants

- Delayed posting that creates a backlog and distorts the trial balance

A 2022 survey from the Clio Legal Trends Report found that 44% of law firm owners reported spending more than two hours per day on administrative and financial tasks. That is time that should be going toward billable work.

Stop the Cycle of Financial Stress: Let a Legal Bookkeeper Handle It

The six steps of the accounting cycle are clear on paper. But when you are managing cases, clients, and compliance at the same time, keeping up with all six steps every single month is a real challenge.

That is exactly where Bookkeeper.law comes in.

Our virtual bookkeeping and staffing services are built specifically for law firms. We do not send you a generalist who has to learn legal accounting on the job. Every virtual bookkeeper we place is trained in legal-specific accounting, trust account management, and bar compliance requirements.

Here is what working with us looks like in practice:

- A dedicated legal bookkeeper assigned to your firm

- Full-cycle accounting management covering all six steps, every period

- IOLTA and trust account reconciliation built into every close

- Seamless integration with Clio, QuickBooks, and PCLaw

- Up to 40% cost savings compared to hiring in-house

You focus on practicing law. We make sure your books are accurate, compliant, and closed on time every single month.

Ready to take the financial stress off your plate?

👉 Schedule a Free Consultation with Bookkeeper.law Today and find out how our virtual legal bookkeeping team can transform the way your firm manages its finances.

https://www.bookkeeper.law/contact

Frequently Asked Questions

What are the six steps in the accounting cycle?

The six steps are: (1) identify and analyze transactions, (2) record journal entries, (3) post to the general ledger, (4) prepare a trial balance, (5) record adjusting entries, and (6) generate financial statements and close the books. Each step builds directly on the one before it, so sequence matters.

What is the main purpose of the accounting cycle?

The accounting cycle ensures every financial transaction is accurately recorded, classified, and reported within a given period. For law firms specifically, it also supports compliance with state bar trust accounting rules and ABA Model Rule 1.15 requirements for client fund management.

How is the accounting cycle different from the budget cycle?

The accounting cycle records and reports what has already happened financially using historical data. The budget cycle plans and forecasts what should happen in a future period. Both are important to a financially healthy law firm, and the accounting cycle is what makes the budget cycle accurate.

Can a law firm outsource its accounting cycle?

Absolutely, and more law firms are doing it every year. Virtual bookkeeping services like Bookkeeper.law manage the full accounting cycle remotely, including trust account reconciliation and compliance-specific reporting. It is a cost-effective, scalable alternative to hiring a full-time in-house accountant.