Unlike traditional business accounting, where write-downs typically involve inventory or equipment, law firm write-downs and write-offs focus on a single primary asset: billable time. Every hour an attorney or paralegal records represents potential revenue, but not all billed time translates into collected fees.

While both reduce the firm’s revenue, they represent distinct billing adjustments that impact your bottom line in different ways. This guide will help you understand the differences between write-downs and write-offs and how to manage them effectively to maintain accurate financial records.

What Is a Write-Down?

A write-down is a voluntary reduction in the amount you bill a client before sending the invoice. It is an adjustment made during the pre-bill review process when you determine that certain time entries should be reduced or adjusted.

When a write-down is used

Write-downs typically occur when you believe the recorded time does not accurately reflect the value delivered to the client.

For example, if your team logged five hours of research at $300 per hour, but the task should reasonably have taken only three hours, you may decide to bill $900 instead of $1,500. The $600 difference is a write-down. The client never sees the original amount—they only receive the adjusted invoice.

Write-downs are also useful for maintaining strong client relationships and securing future business. Firms may apply write-downs as a goodwill gesture for long-standing clients, to remain competitive on pricing, or when the scope of work changes mid-project.

What Is a Write-Off?

A write-off is the removal of an unpaid invoice or accounts receivable balance from your books. It represents an actual revenue loss because the firm no longer expects to collect the outstanding amount.

When you write off an account, you acknowledge that collection is unlikely. The receivable is removed from the balance sheet and recorded as a bad debt expense.

When a write-off is used

Write-offs become necessary when collection efforts have failed and the receivable is deemed uncollectible. This may occur when:

- A client disputes charges and refuses to pay

- A client becomes insolvent or files for bankruptcy

- A client disappears without paying

- An accounts receivable balance ages beyond a reasonable collection period

- The statute of limitations for collection has passed

- The firm chooses to end a contentious client relationship and forgive the outstanding balance

In these situations, the firm has little choice but to write off the balance to keep its financial records accurate.

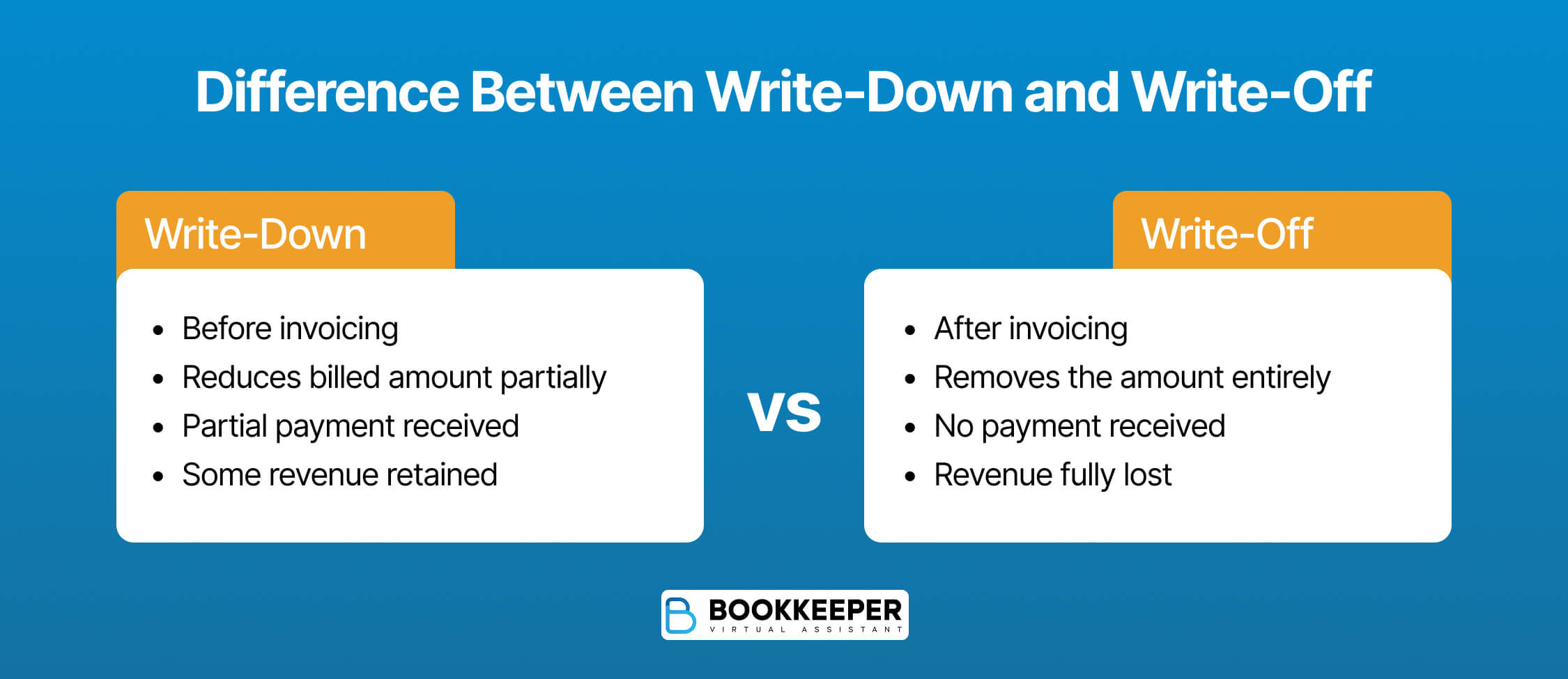

Write-Down vs Write-Off

A write-down is a billing adjustment made before invoicing that reduces the amount charged to a client. The firm bills a lower amount for work performed and receives less revenue but retains some income.

A write-off is a billing adjustment made after invoicing when payment cannot be collected. The firm receives no payment for the written-off amount, resulting in a loss of revenue that was previously recorded or expected.

Write-Down vs Write-Off: Effect on Client Relationship

The decision between writing down time versus writing off receivables often comes down to client relationship strategy. Each approach sends different signals and has distinct implications for ongoing client management.

- Write-downs often strengthen client relationships. They demonstrate that the firm prioritizes fairness over maximizing revenue. This approach works well with clients who closely track legal spend and appreciate transparency and fairness. This goodwill can lead to continued business and referrals.

- Write-offs frequently signal a breakdown in the client relationship. If a firm repeatedly writes off receivables from the same client, it often indicates fundamental issues with that relationship. Red flags include clients who consistently dispute reasonable charges, ignore payment terms, or whose financial situation has deteriorated.

Consideration: When deciding how to handle a billing adjustment, firms should consider the client’s lifetime value. A 20% write-down to retain a client generating $200,000 annually often makes sense. In contrast, writing off a balance for a one-time client with no referral potential may be more practical to avoid collection costs, but it should still lead to a review of billing and intake practices to prevent repeat issues.

Write-Down vs Write-Off: Impact on Law Firm Profitability

Both write-downs and write-offs reduce profitability, but they affect a firm’s books differently.

- Write-downs reduce revenue at the point of billing, but you still collect the remaining billed amount. The loss is limited and predictable, and is more likely to foster repeat business.

- Write-offs are more costly because they result in a complete loss of the billed amount. The firm loses not only the expected revenue but also the overhead costs, staff wages, and time invested in the work.

From a profitability standpoint, a reasonable write-down that preserves a client relationship is almost always preferable to a write-off that eliminates any chance of payment.

How Write-Downs and Write-Offs Impact Realization Rates

Now that we’ve explored the key differences between write-downs and write-offs, let’s look at one of the most critical financial metrics for law firms: realization rates, which measure how much recorded time ultimately converts into collected revenue.

Billing realization

Billing realization measures the percentage of your recorded time that gets billed to clients. Write-downs directly reduce this rate.

- Formula: Billing Realization = (Amount Billed ÷ Amount Recorded at Standard Rates) x 100

- Example: If an attorney records $50,000 in time at standard rates but only bills $42,500 after write-downs, the billing realization is 85%.

Collection realization

Collection realization measures how much of your billed amount is actually collected. Write-offs directly reduce this rate.

- Formula: Collection Realization = (Amount Collected ÷ Amount Billed) x 100

- Example: If the firm billed $60,000 but only collected $35,000 due to write-offs, the collection realization is 58%.

Overall realization rate

Overall realization combines billing realization and collection realization to show the total percentage of recorded time that converts into cash.

- Formula: Overall Realization = Billing Realization x Collection Realization

- Example: 85% × 58% = 49.3% overall realization, meaning more than half of the original recorded value is lost between time recording and collection.

High levels of write-downs or write-offs in either category signal potential problems with pricing, billing practices, or client selection that deserve attention.

Practice area realization rate benchmarks

Trust Account and Retainer Implications

Write-downs and write-offs interact differently with client retainers and trust accounts, creating distinct accounting and ethical considerations.

- Write-downs with active retainers: When a firm holds client funds in trust against future fees, a write-down reduces the amount transferred from the trust account to the operating account. For example, if a client has a $5,000 retainer and the firm writes down a $3,000 bill to $2,500, only $2,500 is transferred to the operating account. The remaining trust balance stays available for future work.

- Write-offs with depleted retainers: Write-offs become more complex once a retainer is exhausted. If the firm bills beyond the retainer and the client does not pay the excess, the firm must write off the unpaid amount. This represents a complete loss of revenue, with no trust funds available to offset it.

Ethical considerations: Bar rules require firms to withdraw only earned fees from trust accounts. A write-down reflects a determination that certain fees were not earned for billing purposes, meaning those amounts remain the client’s property. Firms should clearly document all billing adjustments to maintain accurate trust accounting records and ensure ethical compliance.

In Summary

Understanding the differences between write-offs and write-downs is essential for managing law firm finances effectively. Here’s a quick comparison:

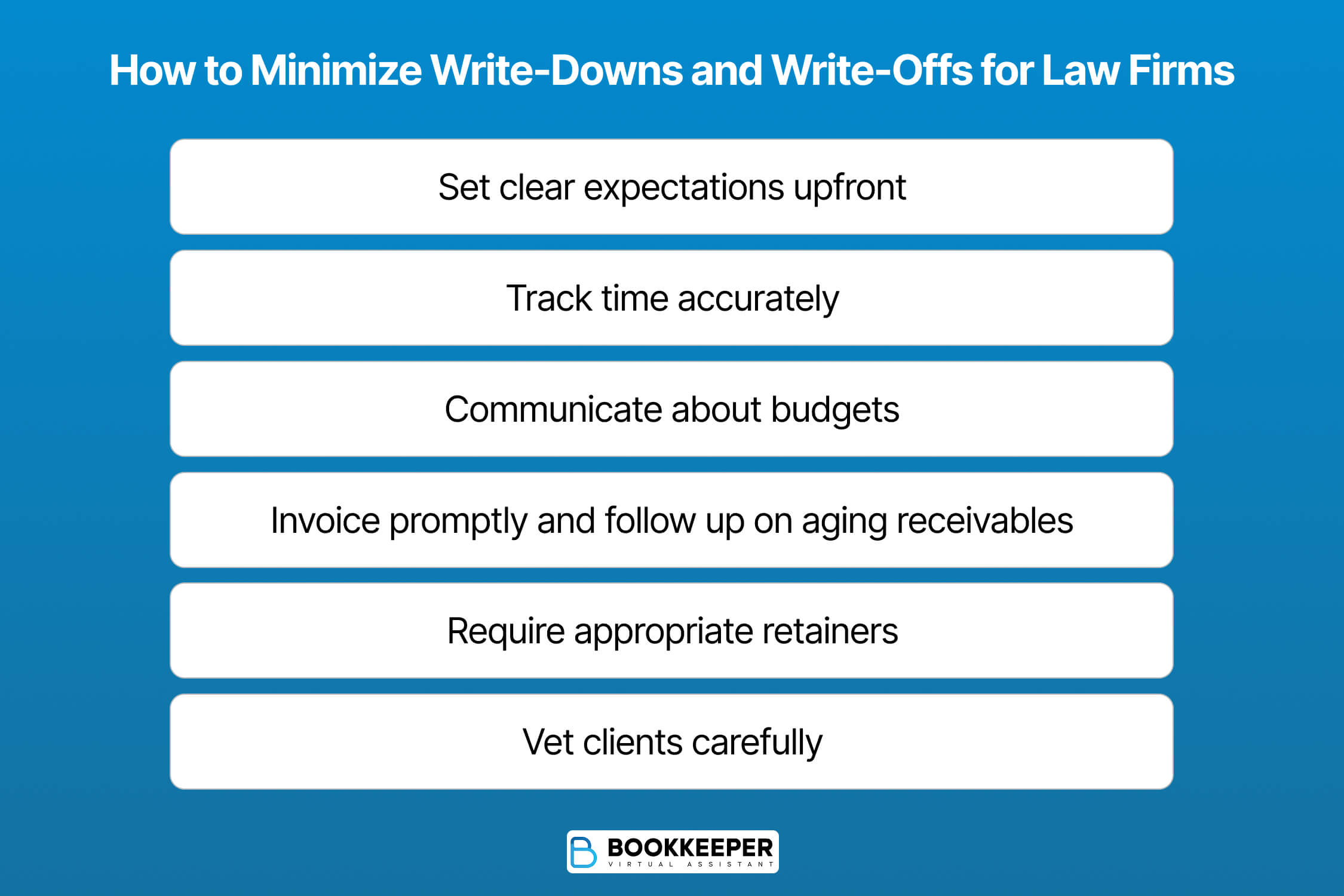

Best Practices to Minimize Write-Downs and Write-Offs

Reducing unnecessary write-downs and preventing write-offs requires attention throughout the client lifecycle. You can achieve this by:

- Setting clear expectations upfront. Use detailed engagement letters that outline the scope, billing rates, and payment terms to prevent misunderstandings that lead to billing disputes.

- Tracking time accurately. Detailed time entries make it easier to justify your bills and reduce the need for write-downs based on vague or excessive-looking entries.

- Communicating about budgets. Inform clients when a matter is trending over budget, it's easier to address issues before invoicing than after.

- Invoicing promptly. Monthly billing keeps receivables manageable and helps identify collection problems early, before balances grow too large to recover.

- Requiring appropriate retainers. Collecting funds upfront reduces write-off risk. Set replenishment requirements to ensure you’re never too far ahead of collected fees.

- Vetting clients carefully. Credit checks and reference calls help avoid clients with payment problems before you invest time in their matters.

- Following up on aging receivables. The longer an invoice goes unpaid, the less likely it is to be collected. Establish a consistent collection process and stick to it.

Ethical and Compliance Considerations

Write-downs and write-offs intersect with several ethical obligations under the ABA Model Rules of Professional Conduct and state bar rules:

Rule 1.5: Fees

Rule 1.5 requires that attorney fees be reasonable. Regular write-downs may indicate that recorded time exceeds what is reasonable for the work performed. Firms should view systematic write-downs as an opportunity to reassess billing practices, staffing efficiency, and matter budgeting.

Rule 1.15: Safekeeping Property

Rule 1.15 governs trust account management. Write-downs affect how much a firm may withdraw from client trust funds. Proper documentation of write-down decisions helps protect both the firm’s interests and the client’s property.

Documentation requirements

Firms should maintain records explaining why write-downs and write-offs occurred. This documentation serves multiple purposes: it supports accurate financial reporting, provides protection in the event of fee disputes or bar complaints, helps identify patterns that may require operational changes, and demonstrates good-faith billing practices.

Avoiding billing fraud

The inverse of write-downs, billing padding, is a serious ethical violation. Firms must ensure that write-downs reflect genuine billing judgment and are not used to mask inflated or unjustified time entries.

Final Note

Managing write-downs and write-offs effectively requires balancing financial discipline with client relationship management. Neither adjustment indicates poor practice; sometimes reducing a bill or acknowledging an uncollectible account is the right business decision.

The goal is to minimize unnecessary adjustments through strong billing practices while recognizing when adjustments are appropriate. Track your metrics, understand your patterns, and make informed decisions that support both your firm’s profitability and your client relationships.

Manage Write-Downs and Write-Offs with Right Professional

If you're looking for a way to get better visibility into your firm's billing adjustments and overall financial health, Bookkeeper.law specializes in helping law firms manage finances by providing legal bookkeepers who understand the unique complexities of law firm accounting and trust accounting rules.

Instead of managing these financial details yourself or relying on a general bookkeeper unfamiliar with legal billing practices, you get a professional who speaks your language and knows what healthy write-down and write-off rates look like for your practice area.

Frequently Asked Questions

What’s a healthy write-down and write-off rate?

Ideally, law firms maintain write-down rates below 10-15% of recorded time and write-off rates below 2-3% of billed amounts. However, acceptable rates vary widely depending on practice area and client base.

What is the effect of writing off a specific accounts receivable?

Writing off an accounts receivable removes the unpaid balance from your firm’s books and records it as a bad debt expense. This reduces your accounts receivable balance on the balance sheet and creates an expense that lowers net income on the income statement. It also acknowledges that the amount is uncollectible, ensuring your financial statements accurately reflect collectible assets.

What is a profit and loss write-off?

This is an accounting entry where an uncollectible debt is moved to the profit and loss statement as an expense. When you write off a receivable, you debit bad debt expense and credit accounts receivable. This reduces taxable income because the revenue was never actually realized.

Do write-offs affect net income?

Yes. Write-offs reduce total revenue and create a bad debt expense on the income statement. This expense is subtracted from revenue along with other operating expenses, lowering the net income available for distributions.