A simple bookkeeping error could cost your healthcare practice millions and destroy patient trust. For instance, recent enforcement actions have resulted in settlements as high as $800,000 for failures in protecting financial data.

One area that often gets overlooked? HIPAA-compliant bookkeeping. Many healthcare providers don't realize that their financial records—such as patient billing details, insurance claims, and payment information—contain Protected Health Information (PHI). Failing to properly secure this data can lead to devastating consequences under a strict penalty structure, with fines for severe neglect reaching up to $2.1 million annually, damaged reputation, and loss of patient trust.

In this guide, we'll break down what HIPAA-compliant bookkeeping actually means, why it matters for your practice, and the practical steps you need to take to protect both your patients and your business.

What is HIPAA-Compliant Bookkeeping?

HIPAA-compliant bookkeeping refers to the financial management practices that healthcare providers must follow to protect patient information while maintaining accurate financial records. This goes beyond simply keeping your books organized, it requires implementing specific safeguards to ensure that any PHI contained in your financial documents remains secure.

Protected Health Information (PHI) includes any individually identifiable health information that relates to a patient's past, present, or future physical or mental health condition, the provision of healthcare to the patient, or payment for healthcare services. In bookkeeping, this often appears in patient billing records, insurance claim details, payment information, and accounts receivable data.

The Department of Health and Human Services (HHS) has investigated over 20,000 HIPAA-related cases since the Privacy Rule was implemented in 2003. As of 2025, approximately 400 healthcare breaches have been reported and are currently under investigation, affecting nearly 30 million individuals. These numbers underscore a critical reality: HIPAA compliance in bookkeeping isn't optional, it's a legal requirement with serious financial consequences.

Why HIPAA Compliance Matters for Your Financial Records

The financial impact of HIPAA violations has reached record highs. In 2024 and 2025, enforcement actions resulted in some of the highest penalties ever recorded, with fines ranging from as little as $25,000 to as much as million for a single violation.

HIPAA violations follow a four-tier penalty structure based on the level of responsibility:

- Tier 1 (Unknowing Violations): Fines range from $137 to $63,973 per violation, with an annual cap of $2 million for repeat violations.

- Tier 2 (Reasonable Cause): Penalties span $1,379 to $63,973 per violation, with similar annual maximums.

- Tier 3 (Willful Neglect, Corrected Within 30 Days): Fines range from $13,785 to $63,973 per violation, with an annual maximum of $2 million.

- Tier 4 (Willful Neglect, Not Corrected): The most serious category, with minimum fines of $63,973 per violation and an annual cap exceeding $2 million.

Beyond financial penalties, healthcare practices face indirect costs that can be even more damaging. Business disruption, patient attrition, increased insurance premiums, legal fees, and corrective action plans add up quickly. Perhaps most importantly, a HIPAA violation destroys patient trust—something that's nearly impossible to rebuild once lost.

Case Study: Common HIPAA Violations in Financial Management

Understanding where violations typically occur can help your practice avoid costly mistakes. Based on recent enforcement data, these are the most common HIPAA violations related to bookkeeping and financial management:

- Unauthorized Access to PHI: Employees accessing patient billing information without proper authorization or business need represent 14.83% of reported breaches. This includes staff members who look up patient records out of curiosity or without a legitimate work-related reason.

- Failure to Conduct Risk Analysis: One of the most frequently cited violations in 2025 enforcement actions. The Office for Civil Rights (OCR) has launched a specific initiative targeting healthcare entities that fail to conduct compliant risk assessments.

- Impermissible Disclosure of PHI: Sharing patient financial information with unauthorized individuals, even unintentionally, violates HIPAA regulations. Memorial Hermann Health System settled for $2.4 million after a staff member improperly disclosed patient information.

- Improper Disposal of PHI: New England Dermatology and Laser Center paid $300,640 for throwing away specimen containers with patient names, birth dates, and provider information without proper disposal protocols.

- Delayed Breach Notification: Oklahoma State University's Center for Health Sciences agreed to pay $875,000 for failing to notify patients within the required 60-day timeframe after discovering a breach.

- Lack of Encryption: Financial data transmitted or stored without proper encryption puts PHI at risk. This includes email communications, cloud storage, and file-sharing practices.

Business Associate Agreements: Your First Line of Defense

If your healthcare practice works with external bookkeepers, accountants, or financial software providers, you need to understand Business Associate Agreements (BAAs). This is where many practices unknowingly expose themselves to HIPAA violations.

A BAA is a legally binding contract between your practice (the covered entity) and any third party that handles PHI on your behalf (the business associate). Under HIPAA regulations, you cannot share PHI with vendors, contractors, or service providers without a signed BAA in place.

Who needs a BAA? Any external party that creates, receives, maintains, or transmits PHI while providing services to your practice. This includes:

- Virtual bookkeepers and accountants who access patient billing information

- Practice management software providers

- Cloud storage services that house financial records containing PHI

- IT professionals who maintain systems with access to patient data

- Billing companies and medical coding services

What should a BAA include? A comprehensive Business Associate Agreement must outline:

- How PHI will be used and disclosed

- Safeguards the business associate will implement

- Breach notification procedures

- Termination conditions

- Return or destruction of PHI when the relationship ends

- Subcontractor requirements if the business associate uses additional vendors

Here's the critical part: without a signed BAA, both your practice and the vendor are exposed to significant regulatory and financial risks. The HHS Office for Civil Rights has clarified that business associates face the same enforcement scrutiny as covered entities. In recent years, OCR has gone after business associates with increased intensity, imposing substantial penalties for non-compliance.

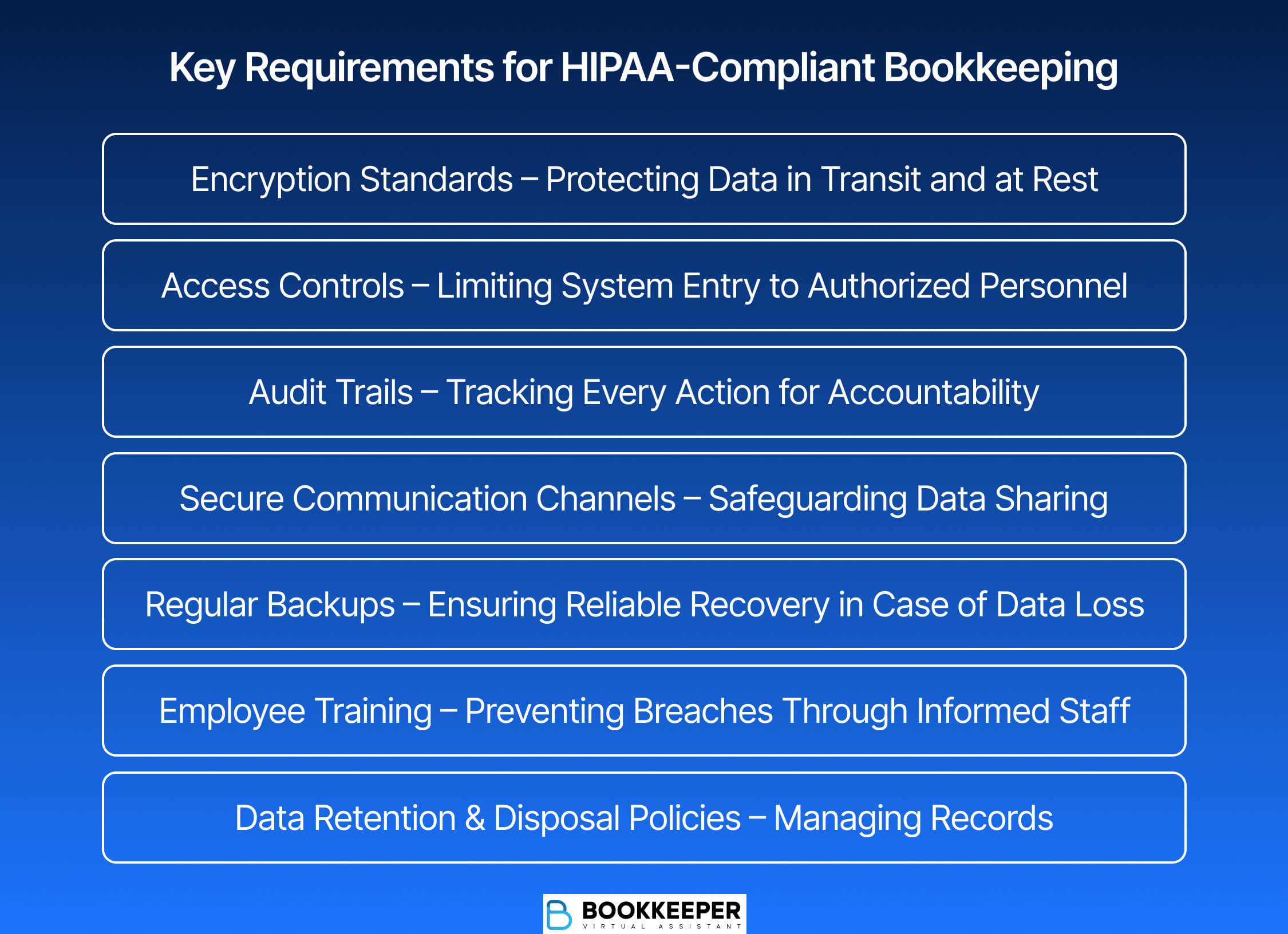

Key Requirements for HIPAA-Compliant Bookkeeping

Maintaining HIPAA compliance in your financial operations requires implementing specific technical, physical, and administrative safeguards. Here's what your practice needs to have in place:

Encryption Standards

Use bookkeeping software and systems that employ AES-256 encryption—the trusted standard that meets HIPAA requirements. Data must be encrypted both at rest (when stored) and in transit (when transmitted). Test your encryption settings regularly to confirm that data cannot be accessed without proper authorization.

Access Controls

Implement role-based access controls that limit PHI access to only those employees who need it to perform their job functions. This follows the "minimum necessary" standard—a core HIPAA principle that requires limiting access, use, and disclosure to the minimum amount needed for the task at hand.

Audit Trails

Your financial systems must automatically track every instance where PHI is accessed. This creates accountability and helps identify potential security issues before they escalate into breaches. These logs should include who accessed the information, when, and what actions they took.

Secure Communication Channels

Never send PHI through regular email or unsecured messaging platforms. Use HIPAA-compliant file-sharing services with end-to-end encryption when sharing financial records with accountants, bookkeepers, or other authorized parties.

Regular Backups

Maintain secure backups of financial records—typically to encrypted cloud storage or external drives. This ensures data recovery in case of system failure while keeping patient information protected.

Employee Training

Conduct regular HIPAA training for all staff members who handle financial records. This should include annual comprehensive training and immediate updates when new regulations or guidelines are issued. Consider implementing phishing awareness programs, as healthcare data breaches increasingly target employees through sophisticated scams.

Data Retention and Disposal Policies

Follow both HIPAA and state-specific guidelines for how long PHI should be retained. When records are no longer needed, ensure secure disposal practices such as digital wiping for electronic records and shredding for physical documents.

Choosing HIPAA-Compliant Accounting Software

Not all accounting software is created equal when it comes to HIPAA compliance. Healthcare practices need platforms specifically designed to handle PHI securely. When evaluating bookkeeping solutions, look for these essential features:

- Business Associate Agreement: The most crucial aspect is whether the vendor will sign a BAA. Without a BAA, the software cannot be considered HIPAA-compliant, period. This is non-negotiable.

- Encryption Capabilities: The platform must use strong encryption (AES-256 standard) for data both in transit and at rest. Verify that the software includes automatic encryption that protects stored data and uses secure protocols like TLS for data transmission.

- Audit Logging: The system should automatically track access to PHI data, creating detailed logs of every instance where sensitive information is viewed, modified, or shared.

- Multi-Factor Authentication (MFA): MFA has become a recommended standard in 2025 for accessing systems containing PHI. This adds an extra security layer beyond just passwords.

- Secure Cloud Infrastructure: If using cloud-based bookkeeping software, confirm that data is hosted in data centers with proper security controls, including perimeter defenses, electronic systems, and building entry point protection.

- Regular Security Testing: Choose vendors that conduct proactive vulnerability testing and have documented incident response plans in place.

Popular HIPAA-compliant options include QuickBooks Online (with a signed BAA), specialized healthcare accounting platforms, and enterprise resource planning (ERP) systems with healthcare-specific modules. Remember that even if software has compliance features, you must still obtain a signed BAA before using it to manage PHI.

Best Practices for Maintaining Financial Compliance

Beyond implementing the right technology, your practice needs to establish ongoing processes that maintain HIPAA compliance in daily operations. Here's how to build a culture of compliance:

- Conduct Regular Risk Assessments: Perform security audits every six months to review access permissions, system settings, and data handling practices. Document all findings and corrective actions taken. This proactive approach helps you spot vulnerabilities before they result in breaches—and it's exactly what OCR looks for during investigations.

- Segregation of Duties: Implement controls that separate critical accounting functions among different team members. This reduces risk by ensuring no single individual has unchecked access to all sensitive information.

- Apply the Minimum Necessary Standard: Regularly review your processes to confirm that staff only access, view, or disclose the PHI strictly required for their specific tasks. Create clear policies documenting what level of access each role requires.

- Monitor Vendor Compliance: Healthcare organizations should reassess third-party vendors annually to ensure ongoing compliance. Consider aligning vendor reviews with your procurement cycle—before paying bills, require vendors to complete updated security questionnaires.

- Document Everything: Maintain comprehensive records of your compliance efforts. HIPAA requires covered entities to retain compliance records for a minimum of six years from the date the record was last in effect. This documentation proves to OCR that you've taken necessary steps to protect data should an investigation occur.

- Establish Clear Protocols: Develop written policies covering data retention, disposal procedures, breach response plans, and employee responsibilities. Make these easily accessible to all staff members who handle financial records.

- Stay Current on Regulations: HIPAA requirements continue to evolve. In 2025, new guidelines emphasize enhanced cybersecurity measures, stronger telehealth security, and updated breach notification procedures. Assign someone in your practice to monitor regulatory changes and update your policies accordingly.

How to Improve Your Practice's Financial Compliance

If you're concerned that your current bookkeeping practices might not meet HIPAA standards, you're not alone. Many healthcare providers discover compliance gaps only after receiving a complaint or during an audit. The good news? Taking action now can prevent costly violations down the line.

Start with a Compliance Assessment

Review your current financial management processes against HIPAA requirements. Ask yourself:

- Do we have signed BAAs with all vendors who access patient billing information?

- Is our bookkeeping software properly encrypted and HIPAA-compliant?

- Have all staff members completed HIPAA training within the past year?

- Do we have documented policies for data retention and disposal?

- Can we prove that we conduct regular risk assessments?

Address Gaps Systematically

If you identify areas of non-compliance, prioritize based on risk level. High-risk issues, like missing BAAs or unencrypted data, require immediate attention. Create a timeline for addressing each gap and assign clear ownership for implementation.

Consider Professional Support

HIPAA compliance can be complex, and oversights are common. Many practices benefit from working with bookkeepers who specialize in healthcare financial management and understand the unique compliance requirements. These professionals already have HIPAA-compliant systems in place, maintain proper training, and can guide your practice toward full compliance.

Invest in the Right Tools

Upgrading to HIPAA-compliant bookkeeping software and secure communication platforms represents a smart investment in your practice's long-term security. While there may be upfront costs, they're minimal compared to the potential penalties and reputation damage from a violation.

Build Compliance into Your Culture

HIPAA compliance shouldn't be seen as a one-time checklist but as an ongoing commitment. When your entire team understands the importance of protecting patient information, even in financial records, compliance becomes second nature.

Secure Your Practice Today

At Bookkeeper.law, we give attorneys the financial support they need to stay compliant, cut costs, and make smarter business decisions. Our legal-trained and pre-vetted virtual bookkeeping professionals specialize in HIPAA-compliant bookkeeping for healthcare, managing everything from signed Business Associate Agreements and encrypted systems to full audit trails. This gives you real-time financial visibility and ironclad compliance, freeing you to focus on patient care.Don't wait for an audit to expose costly compliance gaps that could jeopardize your practice.

Schedule your call today and let us show you how proper HIPAA-compliant bookkeeping protects both your patients and your practice.