Running a business comes with juggling multiple priorities, and sometimes bookkeeping falls behind. Bookkeeping often becomes one of these postponed responsibilities because it feels tedious and time-consuming compared to tasks that directly generate revenue.

What starts as delaying bookkeeping for a few days can easily stretch into weeks, then months. Before you know it, you're facing stacks of receipts, unrecorded transactions, and bank statements that need attention. The situation feels overwhelming, especially when tax deadlines approach or you need financial reports for important business decisions.

You're not facing this challenge alone. Many business owners find themselves in similar situations, and catch up bookkeeping services exist specifically to address this common problem.

What is Catch Up Bookkeeping?

Catch-up bookkeeping is the process of bringing your financial records up to date for past periods you’ve missed. Instead of starting fresh, you catch up on weeks, months, or sometimes even years of financial data that need to be recorded, categorized, and reconciled to bring your books back on track.

This process provides an accurate reflection of your business’s financial position. Think of it as hitting the reset button on your financial records to create a clean, organized foundation moving forward.

When Do You Need Catch Up Bookkeeping?

You might need catch up bookkeeping if your records are incomplete, outdated, or not properly maintained. Here are five common situations where this service makes sense:

1. After Starting Your Business Without Proper Systems

Many entrepreneurs launch their businesses focused on sales and operations, putting bookkeeping on the back burner. If you've been operating for months without properly tracking income and expenses, this leads to gaps that need to be filled before you can understand your financial position. Poor bookkeeping can result in tax errors, penalties, and an increased risk of audits.

2. Following a Bookkeeper Transition

When your previous bookkeeper leaves or you decide to switch accounting professionals, gaps often emerge in your records. The transition period can result in missed entries, incomplete reconciliations, or inconsistent categorization.

3. You haven’t updated your books for months

It’s easy to fall behind when you’re focused on serving clients or running day-to-day operations. If you haven’t touched your books in several months, you probably don’t have a clear idea of your cash flow, and tax season will be more stressful than it needs to be.

4. During Business Growth or Changes

When your business experiences rapid growth, new revenue streams, or operational changes, your existing bookkeeping process may not be able to keep up. Increased transaction volume or complexity can make it harder to stay in control of your finances.

5. Before Tax Season or Audits

If you've neglected regular bookkeeping throughout the year, tax preparation becomes nearly impossible without up-to-date records. If you don’t have your income and expenses in order, you risk last-minute stress, errors, or even penalties.

Who Does Catch Up Bookkeeping?

You have several options for handling catch-up bookkeeping, depending on your budget, timeline, and the complexity of your records.

Some business owners choose to manage it themselves—especially if their transaction volume is low and they have some accounting knowledge. While this DIY approach can save money, it also carries the risk of errors that may lead to costly consequences later.

In-house bookkeepers and accounting firms often specialize in catch-up work. They bring experience with accounting software, follow proper categorization practices, and can efficiently process large volumes of transactions.

Another option is hiring a virtual bookkeeping team. This gives you the same quality of service as an in-house team but at a lower cost. At Bookkeeper.law, our certified bookkeepers work virtually and specialize in helping law firms and small businesses catch up and stay current with their books.

How Much Does It Cost?

Typically, a catch-up bookkeeping service ranges from $200 to $3,000+, depending on several factors. The price is affected by the time period you need to catch up on, the volume of transactions, and the complexity of your current records.

Professional bookkeepers usually charge around $24 per hour. At Bookkeeper.law, we offer simple and transparent pricing, with bookkeeper rates starting at just $14 per hour.

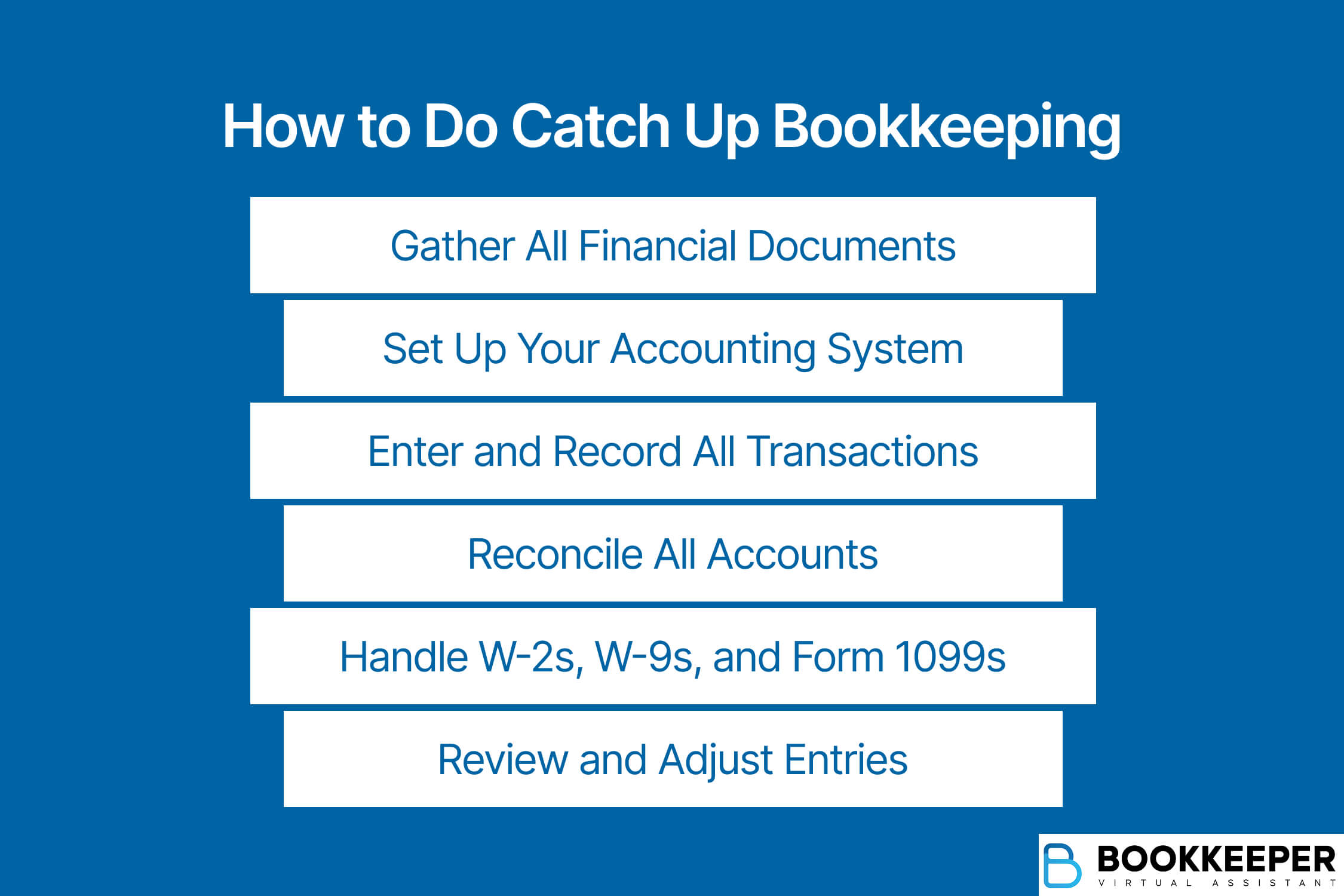

How to Do Catch Up Bookkeeping

If you want to understand the process of keeping your books current, here’s a step-by-step breakdown of what it usually looks like:

Step 1: Gather All Financial Documents

Start by collecting every piece of financial documentation from your catch up period. This includes bank statements, credit card statements, receipts, and any previous bookkeeping records.

The best practice is to create a systematic filing system, either physical or digital, to organize these documents chronologically.

Step 2: Set Up Your Accounting System

Select accounting software that matches your business needs and budget. Popular options include QuickBooks, Xero, and FreshBooks for small businesses. Set up your chart of accounts, which categorizes your income and expenses.

If you're unsure about proper categories, consult with a bookkeeper or use your software's industry-specific templates.

Step 3: Enter and Record All Transactions

Determine your starting point by entering opening balances for all accounts as of the beginning of your catch up period. This includes bank account balances, outstanding invoices, unpaid bills, and any other assets or liabilities.

Work through your financial documents systematically, entering each transaction into your accounting system. Start with the oldest records and work forward chronologically.

Step 4: Reconcile All Accounts

After entering transactions, reconcile each bank and credit card account by comparing your accounting records to the financial institution's statements so you can know your actual financial position. This process identifies discrepancies, missing transactions, or errors that need correction. The balance in your bank statement should end up matching your company records.

Step 5: Handle W-2s, W-9s, and Form 1099s

If you have employees or work with contractors, you'll need to address tax reporting requirements during your catch up process. Ensure all W-2 forms for employees are accurate and filed on time. Collect W-9 forms from contractors and issue 1099 forms for payments exceeding $600 during the tax year. This step is crucial for compliance and helps avoid penalties from the IRS.

Step 6: Review and Adjust Entries

Conduct a thorough review of your completed catch up work. Look for unusual patterns, potential errors, or missing information. Make necessary adjusting entries for items like depreciation, accrued expenses, or prepaid items.

Generate basic financial reports to verify that your numbers make sense for your business type and size.

Final Thoughts

Catch up bookkeeping might feel overwhelming, but it’s a manageable and important step for your business. Whether you choose to handle the work yourself or hire professionals, the key is getting started. The longer you wait, the more complex and expensive the process becomes.

Remember that establishing good bookkeeping habits after completing your catch up work prevents future backlogs and keeps your business financially organized.

Once you're caught up, building consistent bookkeeping habits will help prevent future backlogs and keep your finances organized. Think of it less as an expense and more as an investment in the long-term health of your business. With up-to-date records, you’ll be in a better position to make informed decisions, apply for financing, and plan for growth.

If you're ready to get your books in order, Bookkeeper.law can help you handle the entire process, so you can stay focused on running your business.